Amazon's Ad Billing Change: What the Shift to Proceeds Deduction Means for Cash Flow

Starting August 1, 2026, Amazon is changing how a subset of advertisers pay for Sponsored Products, Sponsored Brands, and Sponsored Display campaigns. Accounts that currently bill ad spend to a credit card will be migrated to proceeds deduction, where advertising costs are netted against your seller balance before disbursement. The change was originally scheduled for April 15 and was pushed back to give sellers more time to prepare.

If you're among the affected sellers, this isn't a fee increase and Amazon isn't charging you more for ads. But it does change when the money leaves your account, and for sellers who relied on credit card billing to manage working capital timing, that shift will be materially important to your business.

This post covers the mechanics of the change, the actual cash flow impact at different ad spend levels, and the steps to take between now and August 1 to keep your capital position intact.

What's Changing and Who's Affected

The majority of Amazon advertisers already pay for ads through proceeds deduction. This change applies only to the subset of accounts that still use a credit card as their primary ad billing method.

After August 1, affected accounts will have two payment options:

Proceeds deduction (the new default). Amazon nets your advertising costs against your seller balance within the disbursement cycle. The cost comes out before funds reach your bank account.

Pay by Invoice (opt-in). Amazon issues a monthly invoice for your ad spend, payable 30 days after month-end. This preserves 30 to 60 days of timing flexibility between when you spend and when you pay.

Credit cards remain on file as a backup method. If your proceeds balance is insufficient to cover ad costs in a given period, Amazon charges the card on file. But credit cards can no longer serve as the primary billing method for affected accounts.

How to check whether your account is affected

If you received a direct email from Amazon or see a billing notification in Campaign Manager, you're in the affected group. You can verify in Ads Console under Billing, then Payment settings. If your account already shows "Account balance" as the primary payment method, you're already on proceeds deduction and nothing changes for you.

How This Changes Your Cash Flow

The mechanical difference is straightforward, but the working capital impact depends on how you were using that credit card.

Under credit card billing, the typical payment cycle worked like this: you incurred ad costs throughout the month, the credit card statement closed at month-end, and payment was due 25 to 30 days later. Meanwhile, Amazon's disbursement cycle released your sales proceeds on a separate schedule. The result was roughly 45 to 60 days between when ad costs were incurred and when cash left your bank account.

Under proceeds deduction, ad costs are netted against your available balance within Amazon's disbursement cycle. The gap between incurring the cost and paying for it shrinks to whatever your disbursement frequency is, typically 14 days for most sellers.

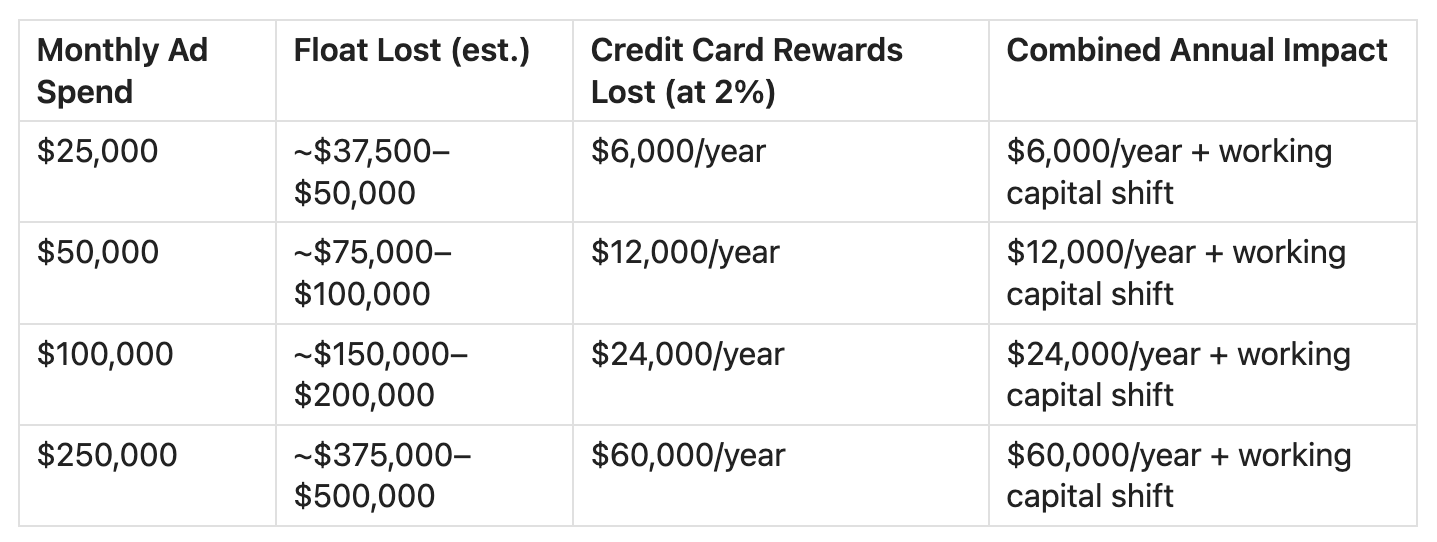

The difference between those two timelines is the float that affected sellers are losing. For a seller spending $50,000 per month on advertising, that float represents approximately $75,000 to $100,000 in working capital that was effectively interest-free.

The math at different ad spend levels

The rewards loss is a real cost, but for most sellers the working capital shift is larger. A seller spending $100,000 per month who loses 45 to 60 days of float needs $150,000 to $200,000 in additional working capital to maintain the same cash position. That capital has to come from somewhere.

This Doesn't Exist in Isolation

The ad billing change lands alongside two other policy updates that also affect cash timing:

DD+7 payout policy (effective March 2026). Disbursements are now calculated from confirmed delivery date plus seven days, rather than ship date plus seven days. Depending on shipping speed, this adds three to seven or more days to your cash conversion cycle. For a seller doing $10,000 per day in revenue, a seven-day delay means $70,000 in additional capital locked in Amazon's disbursement pipeline at any given time.

3.5% fuel & logistics surcharge (effective April 2026). A temporary surcharge applied to FBA fulfillment fees. This is a direct margin impact rather than a timing change, but it compounds the picture for sellers already managing tighter cash flow.

None of these changes affect your ad performance, your organic ranking, or what Amazon charges for advertising. They affect when money moves between Amazon's system and your bank account. The sellers who feel this most are those operating with thin working capital buffers, where a shift in payment timing creates a gap between outflows (supplier deposits, freight, ad costs) and inflows (Amazon disbursements).

For context on how DD+7 specifically affects cash planning, see Amazon's DD+7 Payout Policy: What It Means for Your Cash Flow.

Pay by Invoice: The Option Worth Evaluating

Pay by Invoice doesn't get enough attention in the discussion around this change. It preserves meaningful timing flexibility.

Under Pay by Invoice, Amazon generates a monthly statement for your ad costs. Payment is due 30 days after the end of the billing month. If you spend $50,000 on ads in August, the invoice is issued around September 1, and payment is due around October 1. That's 30 to 60 days from when most of the spend occurred, which is comparable to the old credit card timing for all practical purposes.

It doesn't restore the credit card rewards, but from a working capital timing standpoint, Pay by Invoice recovers most of the float that proceeds deduction eliminates.

How to switch

- Log into Seller Central

- Navigate to Ads Console

- Open Billing, then Payment settings

- Select Pay by Invoice as your default payment method

- Confirm the change

Do this before August 1. Accounts that don't select a preference will be auto-migrated to proceeds deduction.

Who should use which option

Pay by Invoice makes sense if your monthly ad spend exceeds $10,000, you manage cash flow actively across reorder cycles, or the timing flexibility meaningfully affects your ability to fund inventory and ad spend simultaneously.

Proceeds deduction is fine if your ad spend is modest relative to your total revenue, you maintain significant cash reserves, or you prefer the simplicity of having everything netted within a single Amazon disbursement.

How to Prepare Before August 1

The window between now and the effective date is the right time to adjust your capital planning, not after the change takes effect.

Audit your current billing setup. Confirm whether your account is affected and what payment method is currently active. If you're already on proceeds deduction, no action is needed.

Calculate your float exposure. Multiply your monthly ad spend by 1.5 to 2 to estimate the working capital currently supported by credit card float timing. That's the amount of capital you'll need to either replace or plan around.

Evaluate Pay by Invoice. If you spend more than $10,000 per month on advertising, switching to Pay by Invoice before August 1 preserves most of the timing flexibility. It's the closest replacement for the credit card billing cycle.

Adjust your cash flow forecast. If you run a rolling cash flow forecast, model the change in disbursement net amounts starting August. Your disbursements will be smaller by the amount of ad costs deducted, which means less cash arriving in your bank account per cycle. Adjust your reorder timing and supplier payment schedules accordingly. For a framework, see How to Forecast Your Amazon FBA Cash Needs.

Size your working capital buffer. If you don't switch to Pay by Invoice and your float exposure is material, you'll need additional working capital to maintain the same operational flexibility. This could come from retained earnings, a cash reserve, or a line of credit. The key is to have it arranged before August, not after you feel the squeeze in September when Q4 ad budgets start ramping.

Why Q4 Makes This Urgent

Ad spending typically increases 30 to 40 percent during Q4 as sellers compete for holiday traffic. If this billing change takes effect August 1 and you're on proceeds deduction, your first full month under the new system is August. By October and November, your ad spend is at its annual peak, and the proceeds deductions are correspondingly larger.

A seller who spends $100,000 per month on ads normally might spend $130,000 to $140,000 during Q4. Under proceeds deduction, that's $130,000 to $140,000 per month that no longer flows through your bank account before being paid. If you haven't sized your working capital for that scenario, the Q4 ramp becomes the moment the gap becomes acute.

Slope's Amazon Line of Credit

For Amazon sellers who receive an offer through Seller Central, Slope's revolving line of credit* is available directly in the Amazon Lending portal. Revolving lines up to $5M, APRs as low as 8.99%, subject to credit approval and eligibility requirements. Supported by a J.P. Morgan credit facility, originated by Lead Bank, Member FDIC.

Each draw carries a fixed repayment schedule you set at the time of the draw — repayment does not accelerate based on revenue volume. As draws are repaid, the line replenishes for the next inventory cycle. The application uses a soft credit pull and does not affect your personal credit score. No personal guaranty required.

Check your eligibility in the Amazon Lending portal in Seller Central.

*Slope is a financial technology company, not a bank. Business-purpose loans made by Lead Bank and subject to credit approval. Application and consent to obtain personal credit report is required. Subject to minimum revenue and business requirements. Fees vary based on risk assessment and loan term.

Frequently Asked Questions

When does Amazon's ad billing change take effect?

August 1, 2026. The change was originally scheduled for April 15 and was delayed to give affected sellers more time to prepare. Sellers who don't select a payment preference before August 1 will be auto-migrated to proceeds deduction.

Am I affected by this change?

Check Ads Console under Billing, then Payment settings. If you received a direct email from Amazon or see a billing banner in Campaign Manager, your account is in the affected group. If your account already shows proceeds deduction as your primary method, nothing changes.

Can I still use a credit card for Amazon advertising?

Yes, but only as a backup. Credit cards remain on file as a secondary payment method, charged only when your proceeds balance or invoice arrangement is insufficient. They can no longer serve as the primary billing method for affected accounts.

What is Amazon Pay by Invoice for advertising?

Pay by Invoice is a monthly invoicing option where Amazon bills your ad costs at month-end, with payment due 30 days later. This preserves 30 to 60 days of timing flexibility between when you spend and when you pay. You can enable it in Ads Console under Billing before August 1.

How much additional working capital will I need?

Estimate by multiplying your monthly ad spend by 1.5 to 2. That approximates the working capital currently supported by the credit card float. A seller spending $50,000 per month on ads who switches to proceeds deduction would need roughly $75,000 to $100,000 in additional capital to maintain the same cash position. Switching to Pay by Invoice reduces this substantially.

What happens if my ad costs exceed my proceeds balance?

Amazon charges your backup payment method, typically the credit card on file. If no valid backup exists, campaigns may be paused. This is most likely during slow sales weeks, heavy return periods, or early-stage product launches where ad spend is high relative to revenue.

Does this change affect my ad performance or organic ranking?

No. This is a billing change only. Your ad placements, organic ranking, Buy Box eligibility, and campaign performance are unaffected. What changes is when and how the money moves.

Is Amazon offering anything to help with the transition?

Amazon is providing $2,500 per month in advertising click credits for five months ($12,500 total) to affected advertisers, starting August 1. Unused credits do not carry over. At $50,000 per month in ad spend, this represents a 5% offset. At $250,000 per month, it's 1%.

This content is for informational and educational purposes only. It does not constitute financial, legal, or investment advice. Consult a qualified financial advisor before making any borrowing decisions.

Slope is a financial technology company, not a bank. Business-purpose loans made by Lead Bank and subject to credit approval. Application and consent to obtain personal credit report is required. Subject to minimum revenue and business requirements. Fees vary based on risk assessment and loan term.