Why SMB Cash Flow Underwriting Remains Unsolved

The State of Cash Flow Underwriting: Consumers vs SMBs

With the rise of Open Banking in the last few years, there has been significant innovation in consumer cash flow underwriting. Plaid, Nova Credit, Prism, and even Experian have all developed cash flow scores to both rival and complement FICO. Unlike bureau scores, which depend on historical credit activity, cash flow scores capture the live pulse of a borrower’s financials: deposits, withdrawals, recurring streams, and spending behavior as they happen.

As a result, cash flow signals often precede credit activity. Where missed payments don’t appear until after stress has occurred, cash flow events like a drop in income or a ramp up in spending can trigger weeks in advance – being the cause, not effect, of the stress. This makes cash flow data fundamentally different, and therefore highly complementary, to bureau data. Indeed, cash flow underwriting has already enabled many lenders to expand access, right-size credit limits, and manage portfolio-wide risk in real-time.

Yet for SMB lending, progress has been negligible. None of the aforementioned vendors have developed a corresponding score for small businesses. Additionally, no meaningful SMB-native solutions have emerged. Why is that?

The Missing Piece in SMB Lending

The issue is not demand. SMBs represent 43.5% of the U.S. GDP – or about $12 trillion annually. More importantly, financing is existential to business operations in a way that it is not for consumers. Every small business is constrained by working capital, and net terms are woven into nearly every B2B transaction.

Furthermore, SMBs offer a few distinct advantages when it comes to the applicability of cash flow underwriting:

- Bank data is far more available. Unlike consumer underwriting, collecting bank data (via statements or Open Banking) is already standard for most business loan applications.

- There is no FICO. Despite the efforts of many consortiums and bureaus, there is no FICO or Vantage equivalent in the SMB world. More often than not, a business’s credit is fragmented across its own history, its owner(s)’ personal histories, and unreported commercial trades & cash advances – and therefore no single comprehensive score exists.

- Potential to 10x the onboarding experience. The standard SMB underwrite today is a 1 week+ process that depends at its core on laborious, borrower-prepared financials. The standard consumer underwrite today is a 10 second process that depends entirely on bureau-prepared data. Therefore, whereas a 60 second bank connection step adds significant friction to a consumer loan application, it has the polar opposite effect on the business side: the potential to streamline onboarding by orders of magnitude.

And so, a paradox arises. Commercial lending is a massive market. SMBs, in theory, should also be ideal candidates for cash flow underwriting. And yet, no solution exists today. In fact, SMBs today remain the most underserved asset class in credit: too large and complex for consumer products, but too small, too unsophisticated, and too busy for commercial loans. [1]

Why Cash Flow Underwriting for SMBs Remains Unsolved

The real answer is quite simple: SMB cash flows are hard to understand. This is because of 3 distinct characteristics.

Complexity

A consumer typically has a single W2 income stream – which 9 times out of 10 will be identifiable with the keyword DIRECT DEP. A business, by contrast, will often have multiple, distinct income streams ranging from POS sales, to platform payouts, to direct transfers. Financing mechanisms like invoice factoring complicate things further: what appear at first to be new liabilities are in fact advanced payments from outstanding receivables – which we’d often want to consider as revenue, albeit a different kind of revenue.

And income is just the beginning. Business cash flows may also show capital injections, various forms of financing, or personal withdrawals by the owner. Business-personal mixing is quite common to see in sole props: DoorDash deliveries side-by-side with e-commerce payouts, business expenses mixed with personal. And businesses just simply operate more bank accounts, making hidden account detection a critical challenge.

Complexity also plays out across time. Businesses are remarkably dynamic compared to consumers: cash flows can change entirely month-to-month depending on the season, customer demand, supply chain dynamics, and the broader economy. Consider how in just the last few months, U.S. tariffs have completely altered the financials of all importers.

In short, SMB cash flows are not just “more” than consumer cash flows — they are categorically more complex.

Diversity

As much as we fancy ourselves unique, we as consumers are essentially identical from the lens of our cash flows. Consider your expenses: without knowing anything about you, I can bet that this month, you will spend money on food, housing, utilities, transportation, and subscription services, just like every month before. That uniformity lends itself to a simple, global taxonomy that can be captured well by traditional transaction tagging systems (examples from Plaid’s own schema):

- Bank fees

- Entertainment

- Food & drink

- General merchandise

- Home improvement

- Income

- Loan payments

- Medical

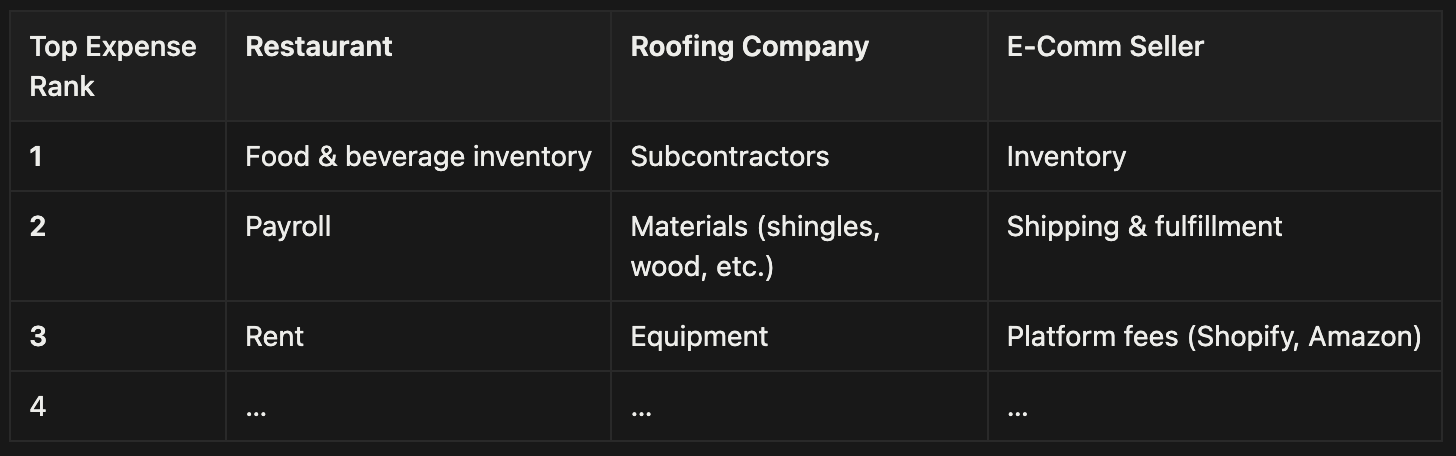

Businesses, by contrast, span dozens of different industries – each of which produce completely different cash flows. Consider the differences between a restaurant, a roofing company, and an E-comm seller: they run completely different business and their cash flows naturally reflect that:

It’s not hard to imagine how a simple taxonomy fails to translate well to the diverse world of business. The existence of CPAs and bookkeeping software that specialize in individual niche industries proves how difficult this is even for humans to solve universally – let alone an automated system.

Context-dependence

Finally, business cash flows are overwhelmingly ambiguous. Consider that a significant portion of a business’s revenue can take the form of ACH transfers, wires, and payments from both individuals and other businesses:

Is it obvious that these transfers are all revenues – as opposed to loans, investments, or personal cash infusions? In certain industries like services or wholesale trade, the entirety of revenue can show up this way. In these cases, traditional NLP engines that operate on individual transaction descriptors may achieve as little as 0% accuracy in income classification. To truly understand business cash flows, this ambiguity can only be resolved using context – such as the nature of the business, the nature of its overall cash flows, or the presence of other similar cash flows. This is not trivial to do reliably.

The Long-Tail Challenge in Business Cash Flow Data

Together, these 3 characteristics – complexity, diversity, and context-dependence – make business cash flow underwriting a classic long-tail problem: one in which a significant portion of the problem lies in a vast number of individual rare cases, rather than a few number of common ones.

In consumer cash flow underwriting, it is an open secret that 3 simple features: income, balance, and overdrafts, derived from simple pattern matching (DIRECT DEP, OVERDRAFT, NSF), can explain the majority loan performance. Not so for SMBs. Complexity, diversity, and context-dependence not only make each individual feature harder to compute (e.g. the revenue examples above), they also make it so that many more features are required to explain the same % of loan performance. Consider a common metric used to underwrite businesses: Debt Service Coverage Ratio (DSCR). The formula for DSCR is:

This single metric depends on 3 specific calculations of income, expenses, and debt – each of which may present completely differently in transactions from industry to industry. And a typical business underwrite will hinge on dozens of such metrics – all of equal importance.

In summary, SMB and Consumer cash flows on the surface look like similar problems but are in fact fundamentally different: one is a short-tail problem, the other is a long-tail problem. The thing that makes long-tail problems hard is that an 80/20 solution does not exist – one must grind out the edge cases one by one, transaction by transaction, counterparty by counterparty.

Tractability — not lack of motive — is the reason we have no SMB cash flow score.

Why Everything Has Changed

In short, Large Language Models. In just the last 3 years, LLMs have mastered natural language, passed the Turing test, and automated entire tasks once thought impossible to automate. Transaction tagging, it turns out, is one of those tasks.

Human-level accuracy

Our research has shown that with careful prompting and fine-tuning, today’s models can achieve SMB transaction categorization accuracy on par with a trained domain expert. Granted, it often isn’t as simple as one-shot inference. Reliability remains a recurring challenge with LLMs: guardrails, data grounding, and fine-tuning are generally musts in a domain with such strict standards for accuracy and explainability. Nonetheless, LLMs provide something qualitatively new: a model class that is broader in knowledge, more adaptable to context, and more general in reasoning than any of its machine learning predecessors .

Software scalability

Unlike human analysts, models can be replicated infinitely. A thousand copies of the same trained “expert” can process years of history in seconds. And advancements in hardware & software make individual LLMs faster and cheaper to run than ever before.

For the first time, we can harness a literal army of human-level domain experts for the modest task of classifying a business’s transactions — at a cost less than a FICO pull. And so, an intractable problem suddenly becomes tractable.

A New Frontier in SMB Lending

At Slope, we have built the first SMB cash flow underwriting system at scale — deployed across some of the largest B2B platforms in the world including Alibaba and Walmart.

At its core is a patented categorization engine powered by Slope TransFormer — a specialized LLM trained to do one thing very well: classify SMB bank transactions. TransFormer takes raw transactions and converts them into a structured, high-dimensional vector of attributes:

In most cases, the model can classify transactions perfectly in a single pass. But as outlined above, context-dependence leaves many transactions that are still too ambiguous — even for a perfectly-tuned LLM. That’s where the additional signals come in. TransFormer generates a number of features that deeply characterize each transaction: the who’s, what’s, how’s, and where’s of the business interaction.

These signals help disambiguate the remaining transactions in two ways:

Semantic contextualization

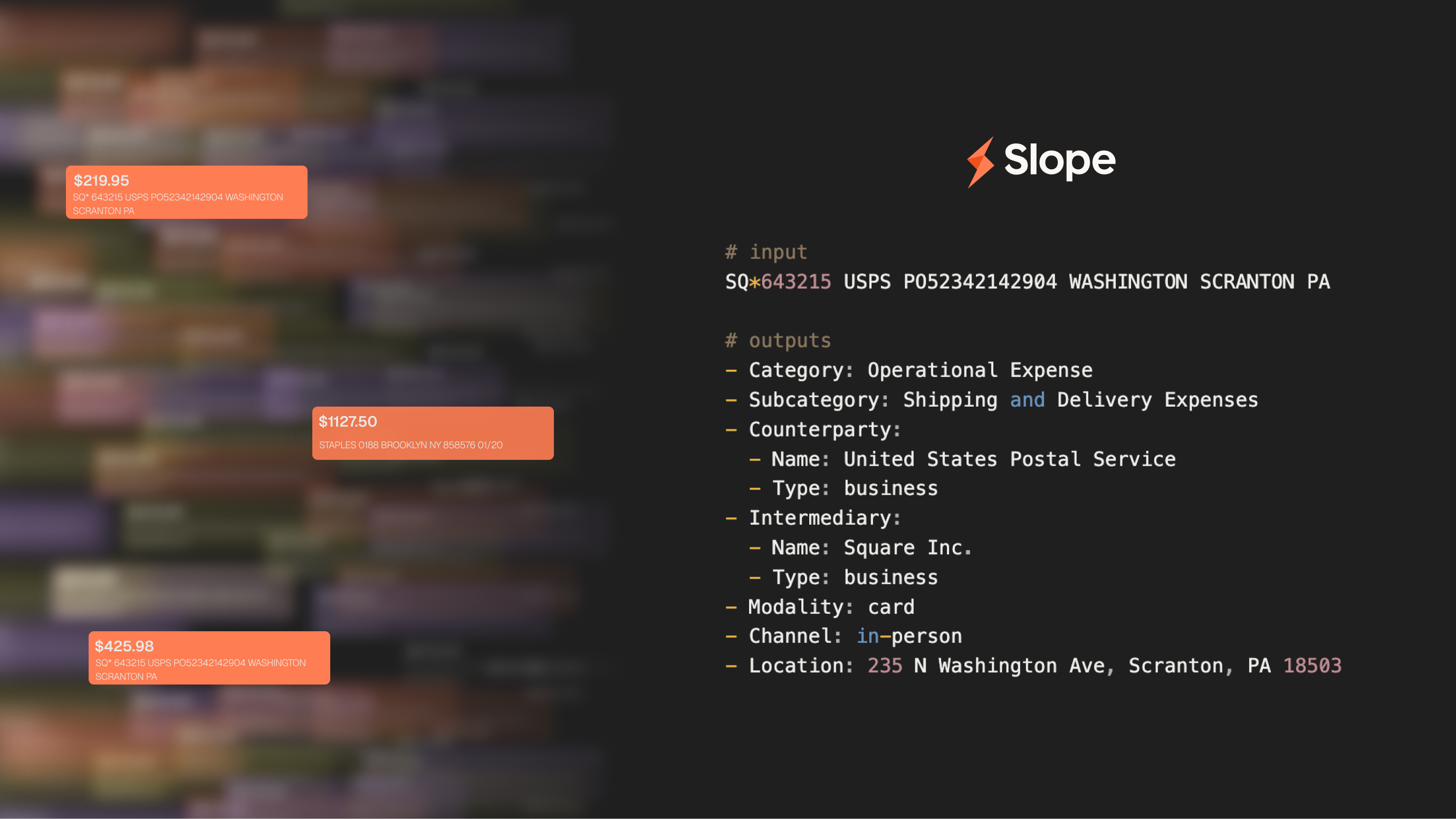

The system uses context clues from the transaction descriptor alongside metadata about the business to resolve ambiguity. Ex)

Firstly, the model recognizes that “SHENZHEN DISTRIBUTORS CORP”, not “MANHATTAN IMPORTERS INC”, is the counterparty, thanks to the knowledge that the latter is the business owner. Secondly, the model makes an inference based on the counterparty, the business name, and the clue: INV#99281 that the transaction is in fact a revenue stream, specifically a B2B revenue stream, rather than a loan, or even another form of revenue.

Statistical contextualization

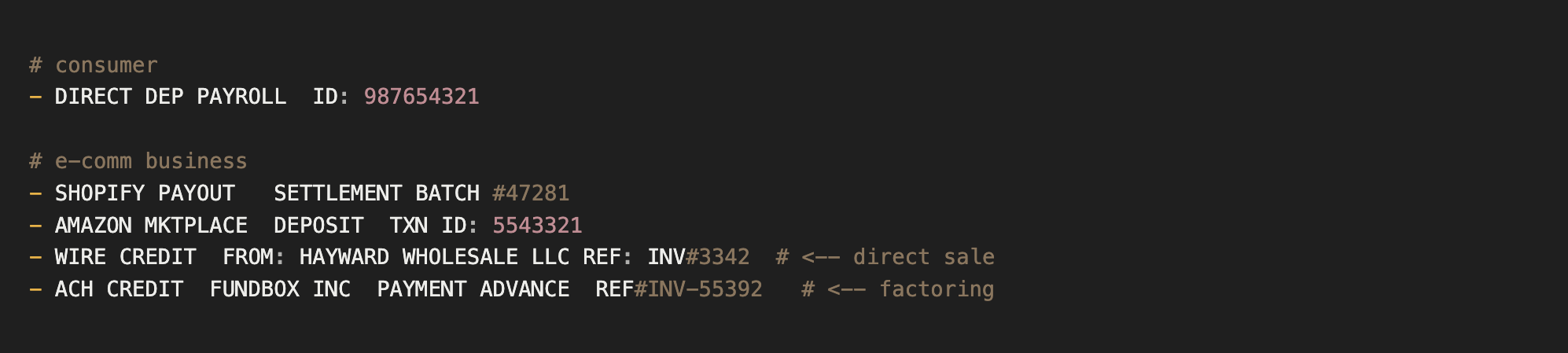

Nevertheless, some transactions remain inscrutable even after semantic contextualization:

In this case, the system will look beyond the transaction towards other similar transactions in high-dimensional space – towards the properties of the overall cash flow: its periodicity, regularity, and recurrence. These properties help us understand the true nature of the cash flow and its significance to the business over time.

The Impact: From Raw Transactions to Reliable Credit Decisions

This is not a prototype. The system described above is live, and to-date has originated close to $500M in business loans. By converting raw transactions into structured signals, it can accurately compute financial features that have traditionally required manual preparation — from income to expenses to debt service coverage ratios. These outputs are robust enough that the system is trusted to make instant approvals of up to $250K based solely on bank data – no financials.

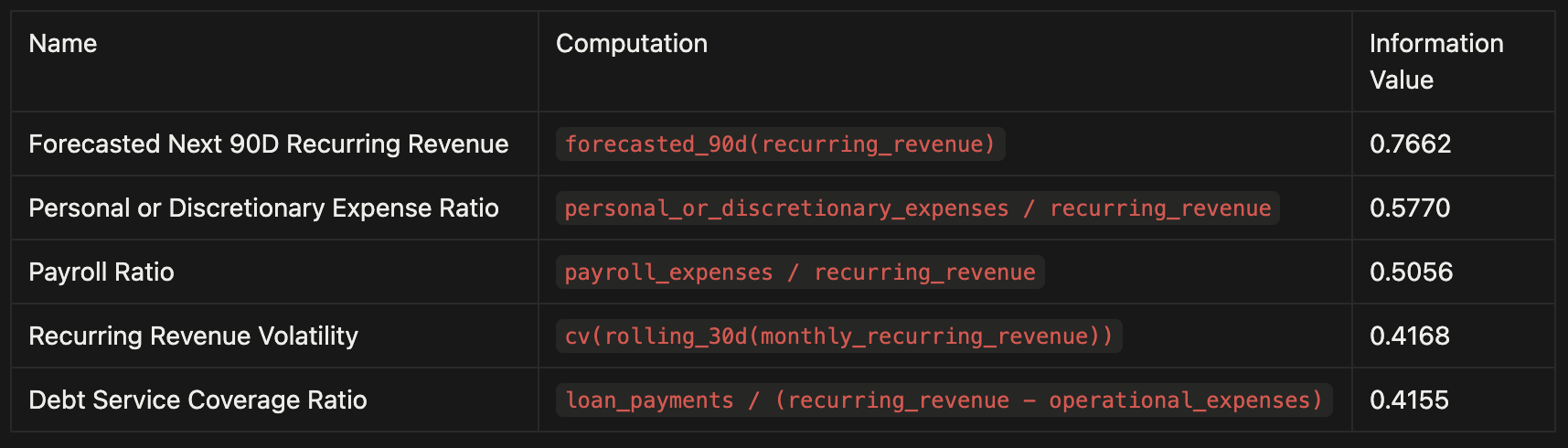

Below are some examples of our most predictive features, their computations, and their associated Information Values (IVs):

These bank-derived financials propagate through the entire underwriting system: from knockout rules, to financial statement reconciliation, to Slope Score: the cash flow probability-of-default (PD) model that ultimately powers lending decisions.

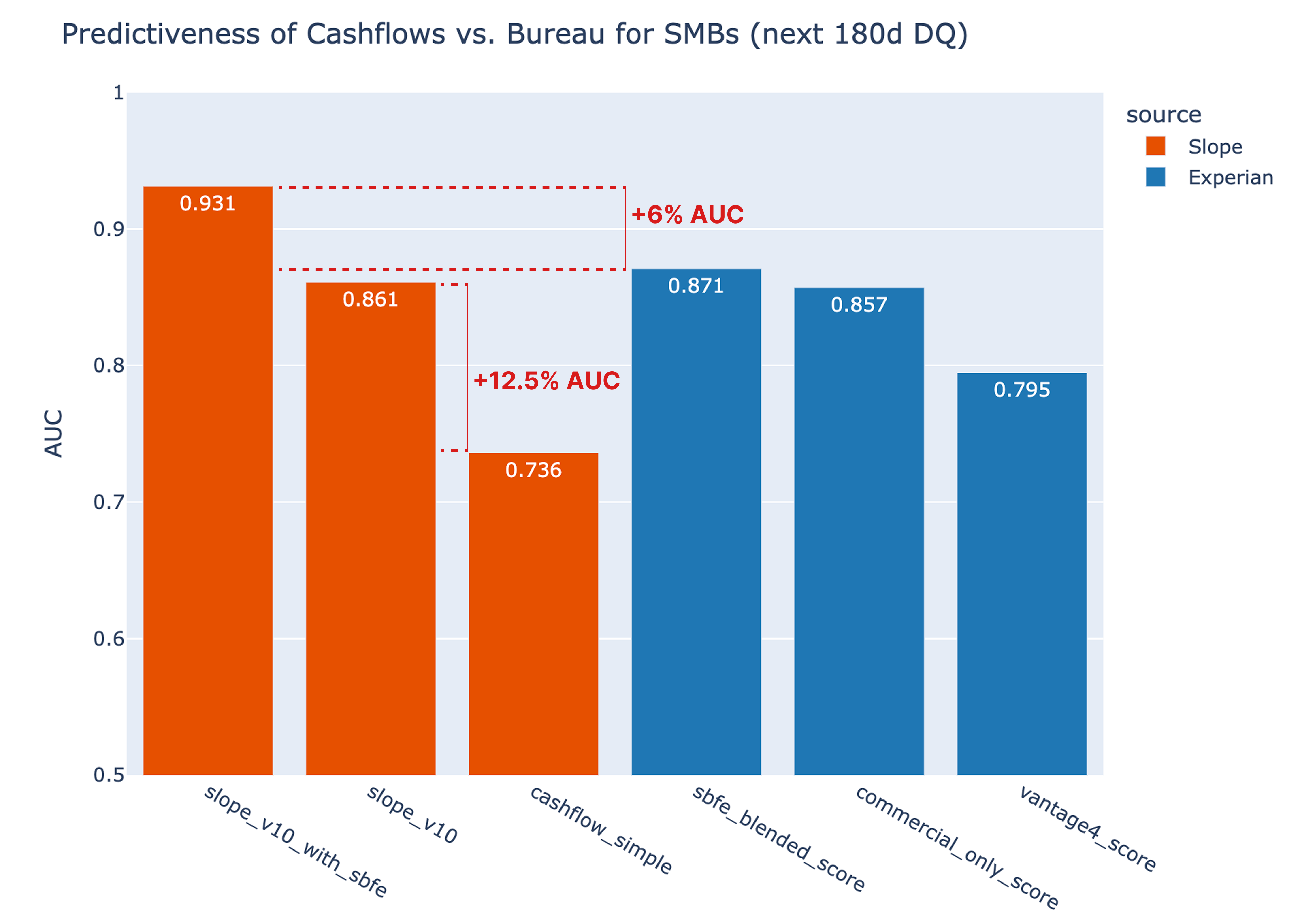

The graph below compares the predictive power of Slope Score vs. 3 popular credit scores provided by Experian:

The results highlight two important truths echoed throughout this post:

- Slope Score vs. SBFE: [+6%] Cash flow underwriting delivers orthogonal value to traditional bureau signals. Even against a comprehensive consortium like SBFE, cash flows add a significant AUC lift — producing a more complete and timely picture of business risk.

- Slope Score vs. Cashflow Simple: [+12.5%] SMB cash flow underwriting is uniquely hard. A simple cash flow model that generally works well for consumers struggles to translate to businesses, because business cash flows are hard. They’re complex, diverse, and context-dependent, and they necessitate the precise, granular features that can only be computed with a modern LLM-centric system.

More in-depth results will soon follow.

The Future of SMB Lending and Cash Flow Underwriting

For decades, the limiting factor in SMB cash flow underwriting has been tractability, not demand. LLMs have changed that equation. Our system, already operating at scale, demonstrates that transaction understanding can be automated with the reliability needed for lending decisions.

This post has laid out the nature of the problem and offered a first look at how it can be addressed. In the coming weeks, we will share more — including more detailed benchmarks and some exciting announcements. For those working on this challenge, or beginning to explore it, we look forward to continuing the conversation.

[1] It’s worth noting that this hole has birthed a new class of payments-native lenders like Square and Stripe, which leverage on-platform data to deliver a far superior UX vs. traditional loans. There is a major drawback, though. These models only see a slice: just the revenues processed on their platform (e.g. Shopify but not Amazon & Walmart) and none of the expenses (e.g. debts, supplier payments, gross margins) – resulting in both missed opportunities and missed risks. Furthermore, they’re platform-dependent – and do not generalize in the same way an open-banking-based system can.