SlopeScore Expands Credit Access With Cash Flow Precision: $868M in New Credit Unlocked

*bank name has been anonymized to protect their privacy

Executive Summary

In a time of accelerating market volatility and increasing pressure to expand credit access responsibly, a top U.S. bank partnered with Slope to explore a new approach to underwriting: real-time cashflow-based scoring. Together, we fine-tuned a cashflow-based underwriting model that:

- Unlocked $868M in new, profitable originations to near-prime and thin-file borrowers from existing customer deposit data, a heavily underserved population.

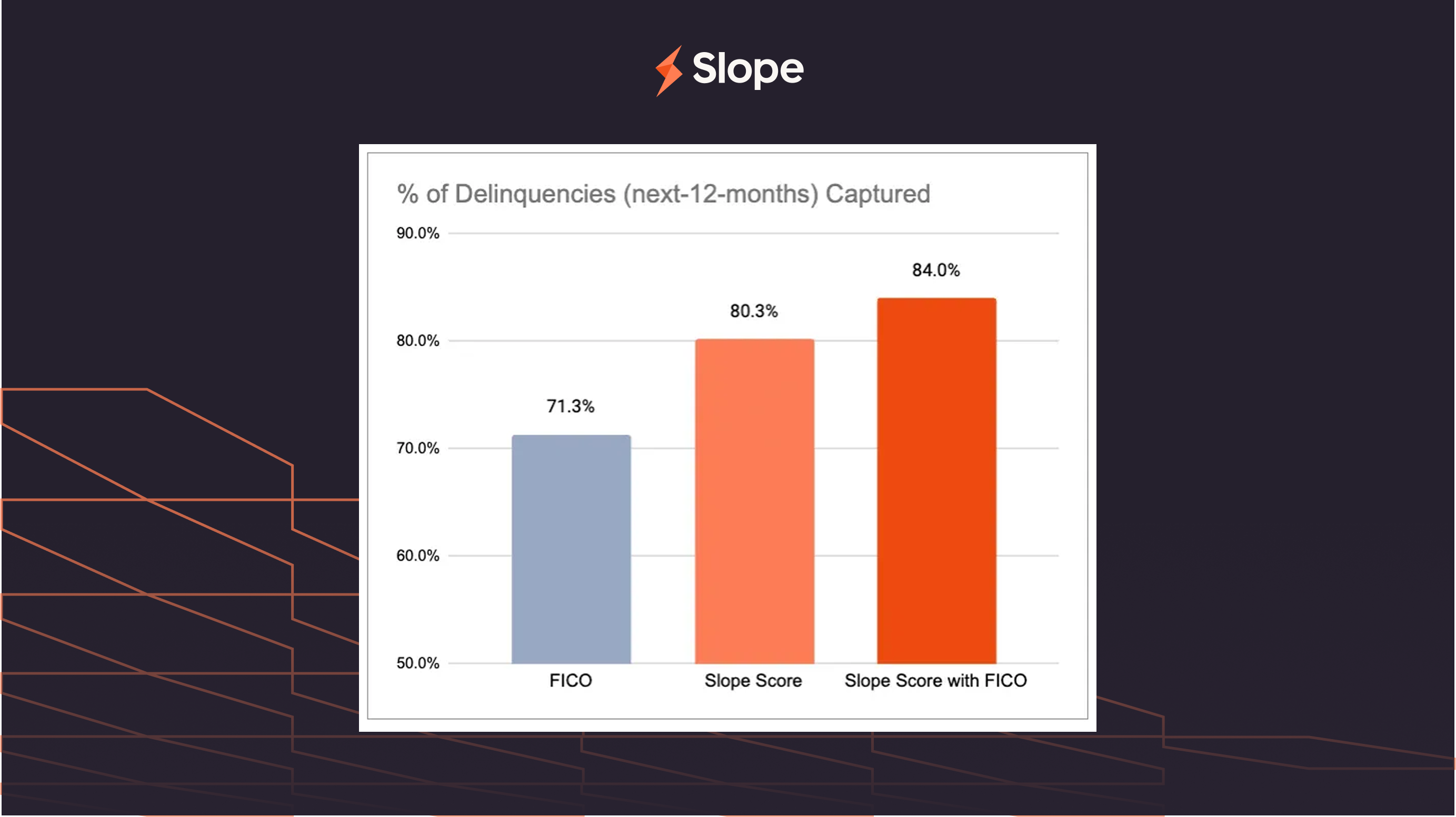

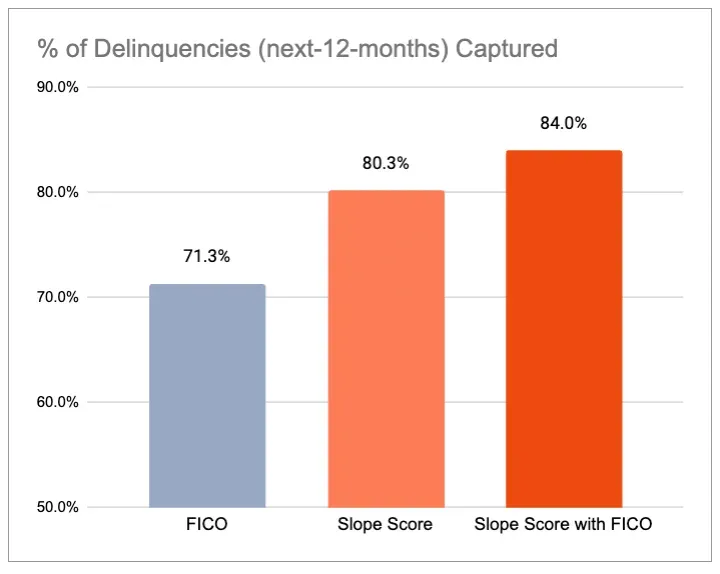

- Outperformed FICO on predicting delinquency in a head-to-head comparison: achieving a bad capture rate of 80% vs. FICO’s 71% – a 14% improvement.

- Achieved 99% categorization accuracy on key features like income, rent, and loan payments – outperforming all other vendors evaluated.

The Problem

Traditional credit scores miss real risk — and real opportunity.The bank has long championed responsible lending and equity in credit access. But traditional tools like FICO don’t always tell the full story — especially for:

- New-to-credit customers (zero FICO)

- Near-prime borrowers which FICO often struggles to rank

- Prime borrowers with recent financial stress – where signals have not yet made it to FICO.

With the rise of open banking – which makes real-time transaction data more accessible than ever before – and the recent breakthroughs of AI, the bank saw an opportunity: by combining access to raw transaction feeds with AI’s ability to process unstructured data at scale, brand new dimensions of credit signals can be unlocked. Signals like income patterns, debt obligations, liquidity, and volatility which aren’t captured in credit reports, and could help paint a more complete, real-time picture of credit worthiness.

The Solution

SlopeScore: Real-Time Cashflow Underwriting

At the heart of this partnership was Slope TransFormer — the first large language model trained to understand bank transactions. Transactions themselves aren’t new — their value has always been clear. However, they are also messy, inconsistent, and deeply contextual, making them historically hard to operationalize. But as complex as transactions are, it turns out they can be framed as a language like English: a domain that modern AI has mastered.

TransFormer understands the language of transactions fluently, identifying counterparties, categories, locations, and payment channels with enough precision to construct detailed, credit-grade features. In a rigorous evaluation of ~6,000 hand-labeled transactions, TransFormer achieved 99% accuracy in key fields like rent, debt, and loan payments – far surpassing all other evaluated alternatives, and in many cases correcting labeling mistakes made originally by humans.

On top of the computed features, the bank and Slope jointly fine-tuned an underwriting model on 15,000 credit card consumers with real, payment performance data. The result: a SlopeScore that covers 100% of applicants (including those without FICO), updates daily, and captures risk signals missed by FICO.

Slope and the bank worked closely across compliance, credit, and data teams to validate features, align to credit policy, and ensure the model met fairness and explainability standards. Deployable alongside existing systems, the model is meant to complement – not replace – existing signals such as FICO.

Results

Accuracy (18 month prediction)

- FICO Bad Capture Rate: 71.3%

- SlopeScore Bad Capture Rate: 80.3% (+9%)

- Combined Bad Capture Rate: 84.0% (+12.7%)

- SlopeScore has low correlation with FICO, thanks to capturing orthogonal, leading signals.

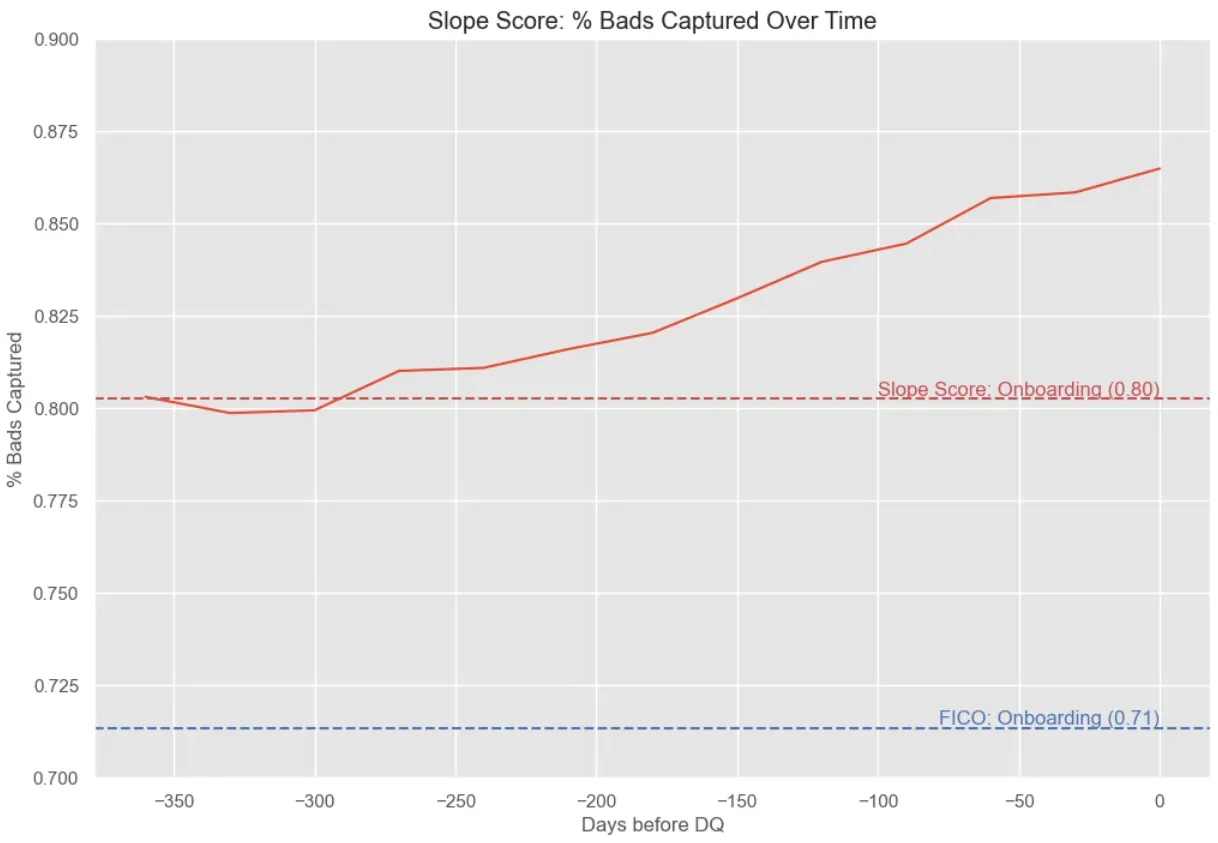

Monitoring (60 day prediction)

- SlopeScore Bad Capture Rate: 85.7% (+14.4%)

- Enables early warning triggers post-origination, refreshed daily with live transaction feeds.

Business Impact

- $868M in new originations identified — to thin-file and near-prime borrowers previously denied due to lack of history

- 14% increase in bad capture rate at same approval threshold

- Precise Risk Stratification: SlopeScore identified prime customers with above average loss rates due to stressed cash flows. And thin-file customers with prime performance.

- Powerful companion to FICO: with low correlation to FICO, SlopeScore helps capture orthogonal, leading risk signals computed from live transaction data. When combined, FICO and SlopeScore maximize access while keeping losses airtight.

What This Means for the Industry

These results signal more than better credit decisions — they reflect a structural shift in how lenders assess and serve customers. Cashflow underwriting doesn’t just improve outcomes at the edges — it reshapes the decision boundary, allowing thin-file, near-prime, and overlooked segments to be underwritten with confidence using ground-truth financial data.

In the near term, this enables forward-thinking banks to safely expand into markets competitors can’t reach — younger borrowers, gig workers, and emerging SMBs. Lending becomes more precise, with dynamic monitoring, early risk signals, and real-time pricing — unlocking a more agile credit lifecycle. Longer-term, it marks the start of real-time, responsive finance: credit that adapts automatically to a business’s needs, performance, and risk profile.

For banks, this creates a smarter, more resilient infrastructure. For the industry, it advances inclusion without sacrificing performance. This isn’t just automation — it’s a new operating model for lending. And for early adopters like this bank, it’s a chance to lead the next era of credit.